General advice warning:

The information contained in this report is for information purposes only and makes no recommendations. It has not taken into account your personal circumstances and situation and accordingly, it is not financial product advice and should not be relied upon as financial product advice. Please speak with a financial adviser before making any investment decisions.

How Much is enough?

The million-dollar question – how much do we need in retirement?

Obviously, there is a not a one answer fits all approach that can be provided as there are so many different factors that need to be considered on an individual bases.

To get to this answer we need to ask more questions:

These are the 20 questions every retiree, or want to be retiree, should be asking:

- How much income do I need in retirement?

- How much capital do I need to retire?

- Will you retire completely or semi retire for a period?

- Do you want to grow your capital in retirement?

- Are you happy to drawdown your capital in retirement?

- What assets are you prepared to sell to fund your retirement, and do you need to sell any at all?

- Are you wanting to stay in your home in retirement or are you prepared to downsize?

- How will you fund aged care and are you open to retirement community living?

- What are you going to do with your time? Travel? Activities?

- What is your passion and how much have you allocated to explore this?

- What will you do if you suffer the loss of a spouse?

- What will you do if one of you suffer a debilitating illness sick?

- What exercise or activity are you going to commit to and be active?

- What social interactions are you going to commit to and be socially fulfilled?

- What commitment to regular medical check-ups will you make to yourself?

- How much are you prepared to be tied to helping the grandkids?

- Do you have a professional team to help you with your finances as you age?

- Are you comfortable with an online solution for your superannuation?

- Should you retire? Or are you happy working…it is ok.

- Who are you working with to keep you accountable on all of these things?

From here is where we work with clients to help put the financial pieces together of the retirement puzzle to determine a realistic number that will help you achieve your ideal life in retirement.

When thinking about how much you will need to live on in retirement, there is a vast array of information on the internet that can help get you started.

For this month’s show I did my own google searches and have sourced information from sites such as ASFA, ASIC, Canstar and the ABS. Following are some snippets that I found, and it will show you a little bit about what you can find to help you get to that final number.

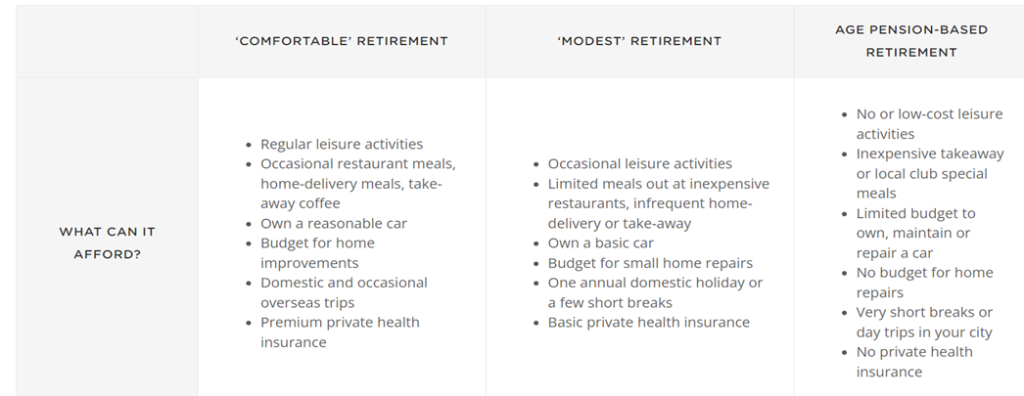

The first question to ask ourselves is, what sort of lifestyle do we want in retirement? Everybody is different and it will change on a case by case basis. So for the purposes of this conversation, we’ve found some very broad, general definitions on on lifestyles, courtesy of The Australian Institute of Health and Welfare and the Association of Superannuation Funds of Australia (ASFA).

ASFA provides us with three broad groups: comfortable, modest and age-pension based.

The Australian Institute of Health and Welfare showed the following helpful information:

A Comfortable versus Modest versus Age Pension based Retirement

Determining the amount of superannuation needed to retire in Australia depends on various factors, including your desired lifestyle, retirement age, and whether you own your home. Here’s an overview based on the latest data from the Australian Securities and Investments Commission (ASIC), the Australian Bureau of Statistics (ABS), and Services Australia. Home – Moneysmart.gov.au

Please note, these figures are based on the Association of Superannuation Funds of Australia’s (ASFA) estimate of howe much money is needed in retirement, depending on your lifestyle. They were updated as of the September quarter 2024 and can be found on Moneysmart.gov or at https://www.superguru.com.au/retiring/how-much-super-will-i-need

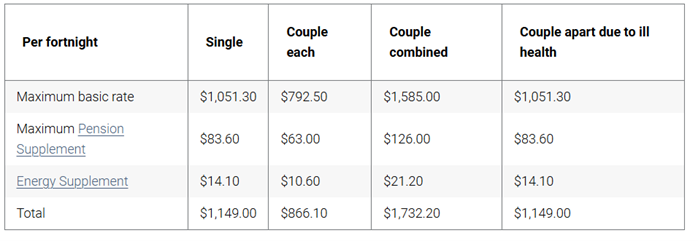

Note: Current Pension rates in Australia:

Assuming you were to qualify for the full rates, this would equate to the following annual figures:

- A single would receive $29,874 per annum.

- Couples would receive $45,037 (combined per annum).

https://www.servicesaustralia.gov.au/how-much-age-pension-you-can-get?context=22526

💰 Superannuation Targets for Retirement

(Note: we think these targets are way too low)

- Modest Lifestyle

- Single: Approximately $100,000 in superannuation.

- Couple: Approximately $150,000 in superannuation.

- This assumes homeownership and eligibility for the Age Pension. Services Australia+11news+11Services Australia+11

Estimated Annual Income (including Age Pension):

- Single: ~$31,000–$33,000

- Couple: ~$45,000–$48,000

✳️ This would support basic expenses, health care, and occasional leisure, but no overseas travel or luxuries.

- Comfortable Lifestyle

- Single: Approximately $595,000 in superannuation.

- Couple: Approximately $690,000 in superannuation.

- This allows for a lifestyle that includes leisure activities, private health insurance, and occasional travel. news+2The Australian+2The Australian+2Home – Moneysmart.gov.au+1The Guardian+1

Estimated Annual Income (including part Age Pension):

- Single: ~$51,000–$53,000

- Couple: ~$72,000–$75,000

✳️ Covers leisure activities, private health insurance, domestic and some overseas travel, home maintenance, and a reasonable buffer for unexpected costs.

- High-Expenditure Lifestyle (we think this is what most households with 2 working parents would aim for)

- Single: Approximately $876,000 in superannuation.

- Couple: Approximately $1,223,000 in superannuation.

- This supports a more luxurious retirement with higher annual spending. news

Estimated Annual Income (self-funded):

- Single: ~$65,000–$70,000

- Couple: ~$90,000–$100,000

✳️ Enables a more luxurious lifestyle, regular international travel, premium private health, home upgrades, dining out, and generous discretionary spending.

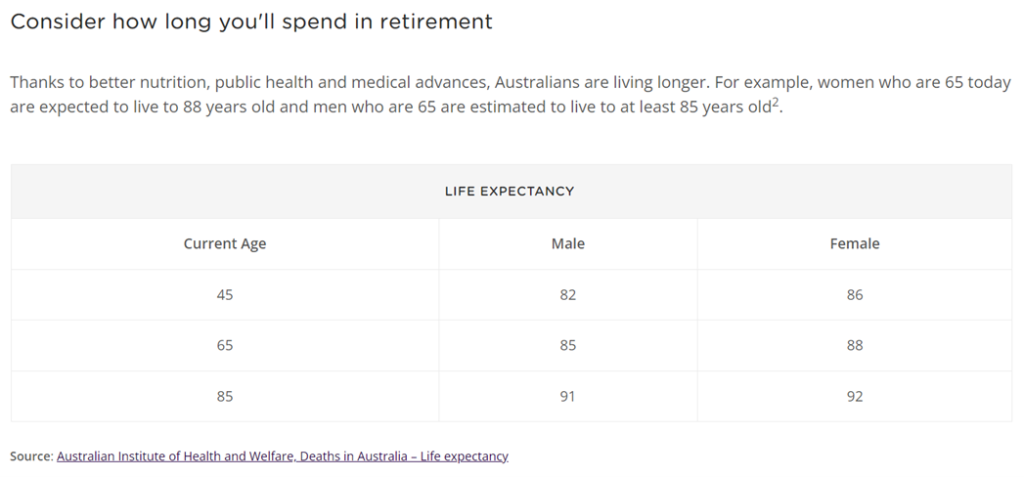

📊 Retirement Age and Life Expectancy

- Average Intended Retirement Age: 65.4 years.

- Average Life Expectancy: Approximately 85 years.

- This suggests retirees need to plan for at least 20 years of retirement income. Home – Moneysmart.gov.au+5Australian Bureau of Statistics+5Australian Bureau of Statistics+5The Guardian+6Home – Moneysmart.gov.au+6Home – Moneysmart.gov.au+6

🧮 Tools for Planning

- Moneysmart Retirement Planner: Helps estimate how much superannuation you’ll have and need.

- Superannuation Calculator: Assists in projecting your super balance at retirement. Home – Moneysmart.gov.au+14Home – Moneysmart.gov.au+14Home – Moneysmart.gov.au+14Home – Moneysmart.gov.au+9Home – Moneysmart.gov.au+9Home – Moneysmart.gov.au+9

🏡 Homeownership and the Age Pension

- These estimates assume you own your home.

- The Age Pension can supplement retirement income, but eligibility depends on income and assets tests. Home – Moneysmart.gov.au+1news+1Home – Moneysmart.gov.au+5Services Australia+5Services Australia+5

📈 Inflation and Cost of Living

- Rising costs, especially in insurance, electricity, and food, have increased the annual expenses for a comfortable retirement.

- As of recent data, couples aged 65 need to spend approximately $72,000 annually to maintain a comfortable lifestyle. The Australian+1news+1

Using the Superannuation targets provided earlier, here’s a breakdown of the approximate annual income each superannuation balance might support during retirement. These estimates assume:

- Retirement age of 67

- Life expectancy of 87 (20 years in retirement)

- 5% average net investment return

- 2.5% inflation (for real income preservation)

- Drawdown using ASFA’s recommended methodology (Association of Superannuation Funds of Australia)

- Figures are in today’s dollars, assuming homeownership and partial or full Age Pension support where applicable.

These projections are based on conservative drawdown strategies aimed at making super last through a 20-year retirement.

YOU NEED TO NOTE: The government sites all actually rely on you spending the capital down

While the required superannuation amount varies based on individual circumstances, these benchmarks provide a general guide. It’s essential to regularly review your retirement plan, considering factors like inflation, investment returns, and changes in personal circumstances. Remember that most government sites that show projections have you spending your capital down over time.

High-Net-Worth Individual (HNWI)

In Australia, an HNWI is generally someone with investable assets over $2.5 million, excluding their family home. For our superannuation example, we’ll focus on someone with $2 million in superannuation.

🧾 Estimated Retirement Income (Self-funded)

Assuming:

- $2,000,000 superannuation balance

- 5% net return

- 2.5% inflation

- Drawdown over 20 years (age 67 to 87)

- No Age Pension eligibility (due to wealth test)

🔹 Estimated Annual Income:

≈ $115,000 – $130,000 per year (in today’s dollars, inflation-adjusted)

Note: Income could be higher with riskier asset allocation or longer drawdown horizon, but this assumes a conservative, sustainable drawdown rate (~5.5%-6.5%).

🌟 Lifestyle Summary at This Level

A retiree with $2 million in super could expect a premium lifestyle that includes:

- First-class private health cover

- Frequent international travel

- Dining out and entertainment

- Significant discretionary spending

- Regular gifts or financial support to family

- Professional advisory services (legal, tax, financial)

- Upgrades or renovations on home/holiday properties

- Ability to donate or invest in philanthropic causes

This lifestyle generally reflects well above the “comfortable” standard and offers financial independence with significant buffer room for longevity, market shocks, or increased care needs later in life.

The Government has a free site: moneysmart.gov.au with a lot of useful financial information.

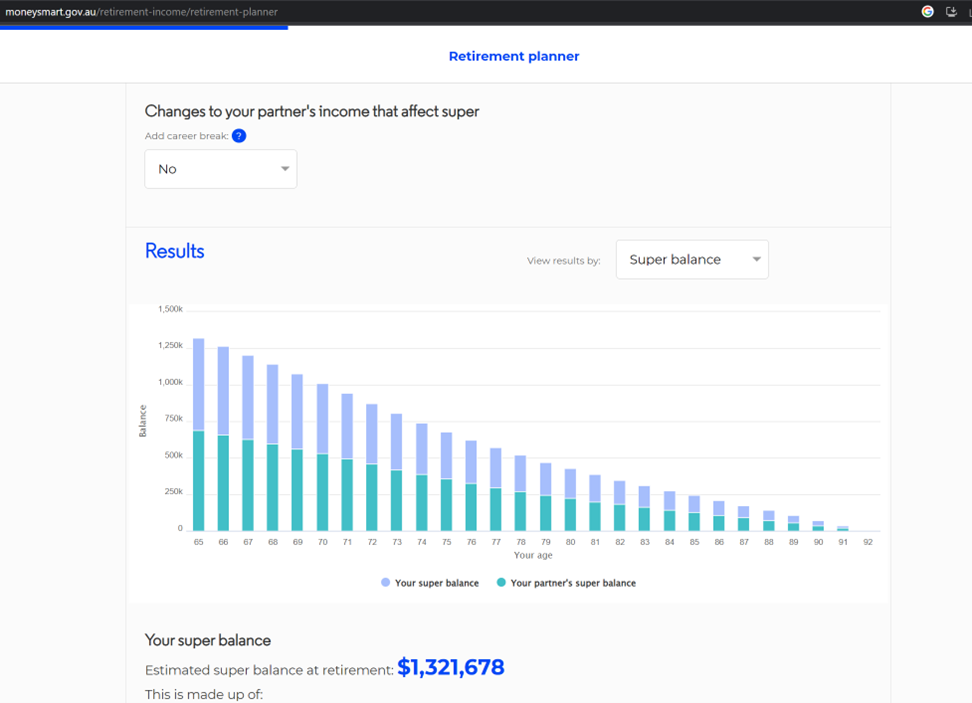

I reviewed a few of the different calculators that they have available. In relation to retirement planning, they have a calculator on how much super you will need based on different income needs.

I tried a few different input options to see what it came up with. If you are going to use this yourself, be aware that it does assume that you are comfortable to drawdown on your capital. This is the case for a lot of people but others want to live off the income and maintain their capital and help the next generation. Neither is a hard and fast rule it is just what works for you and your desired outcome.

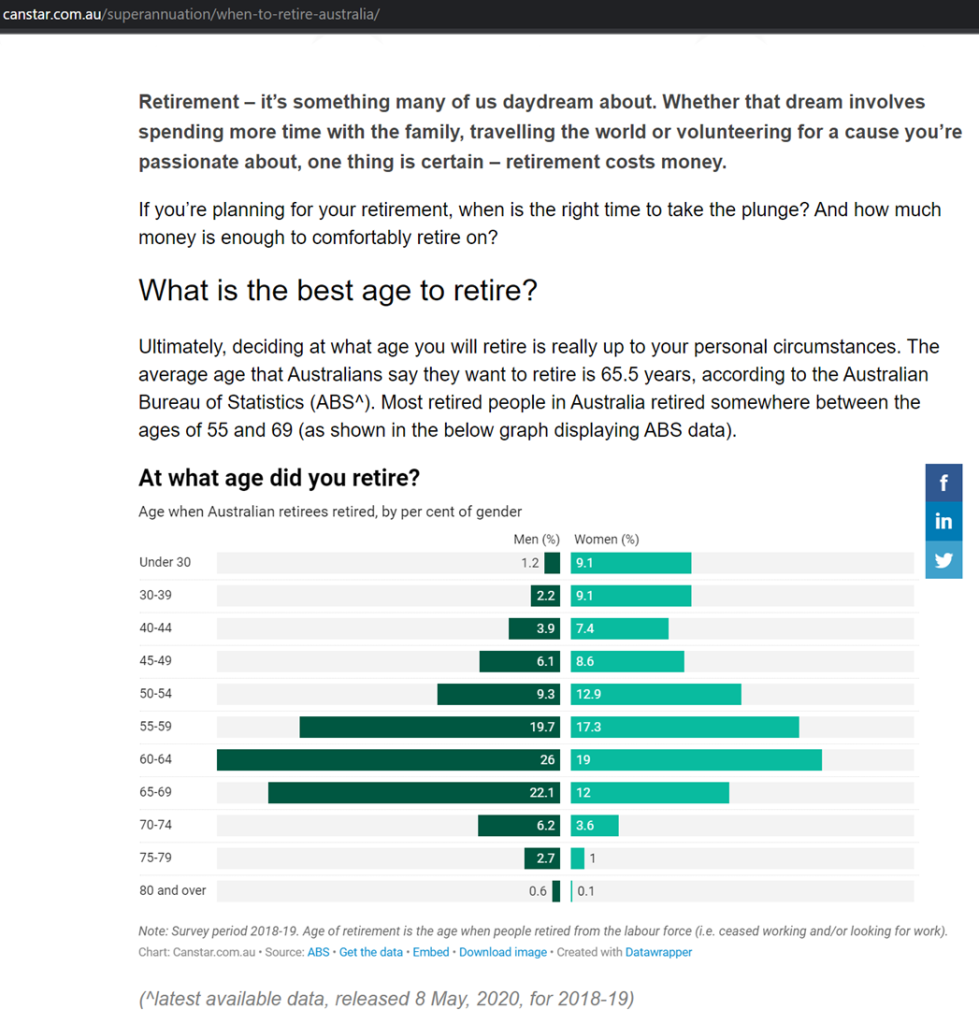

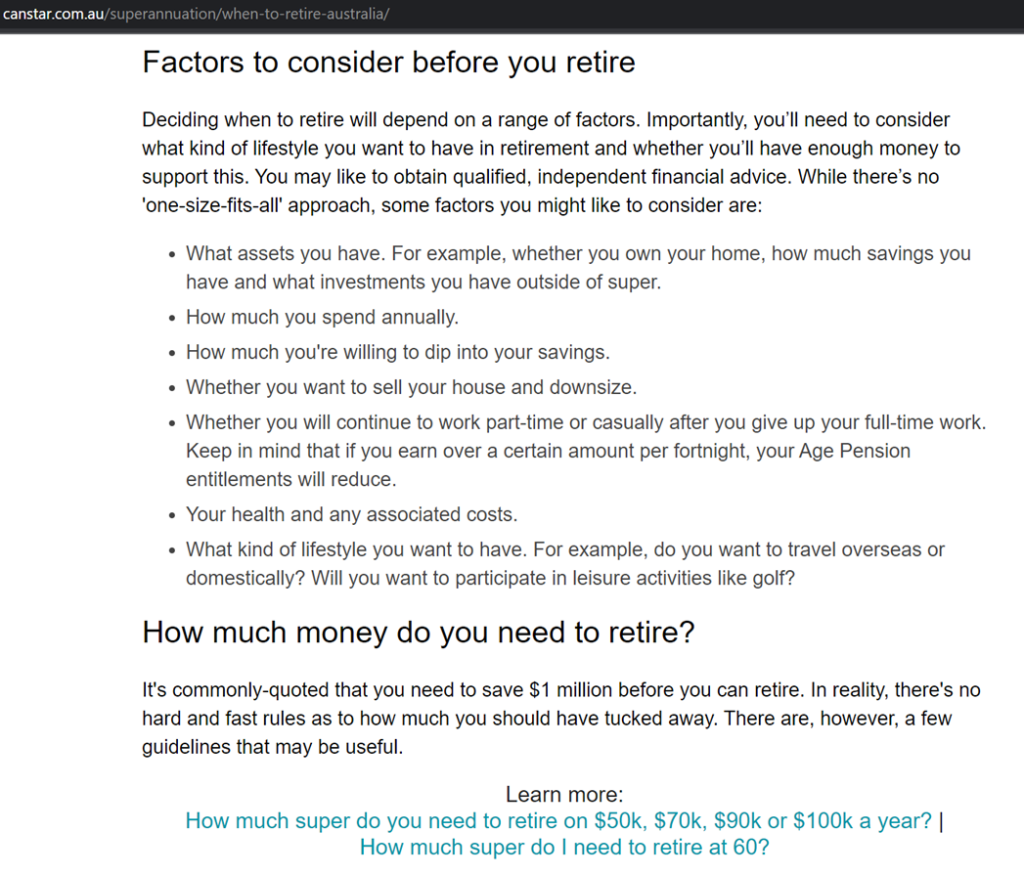

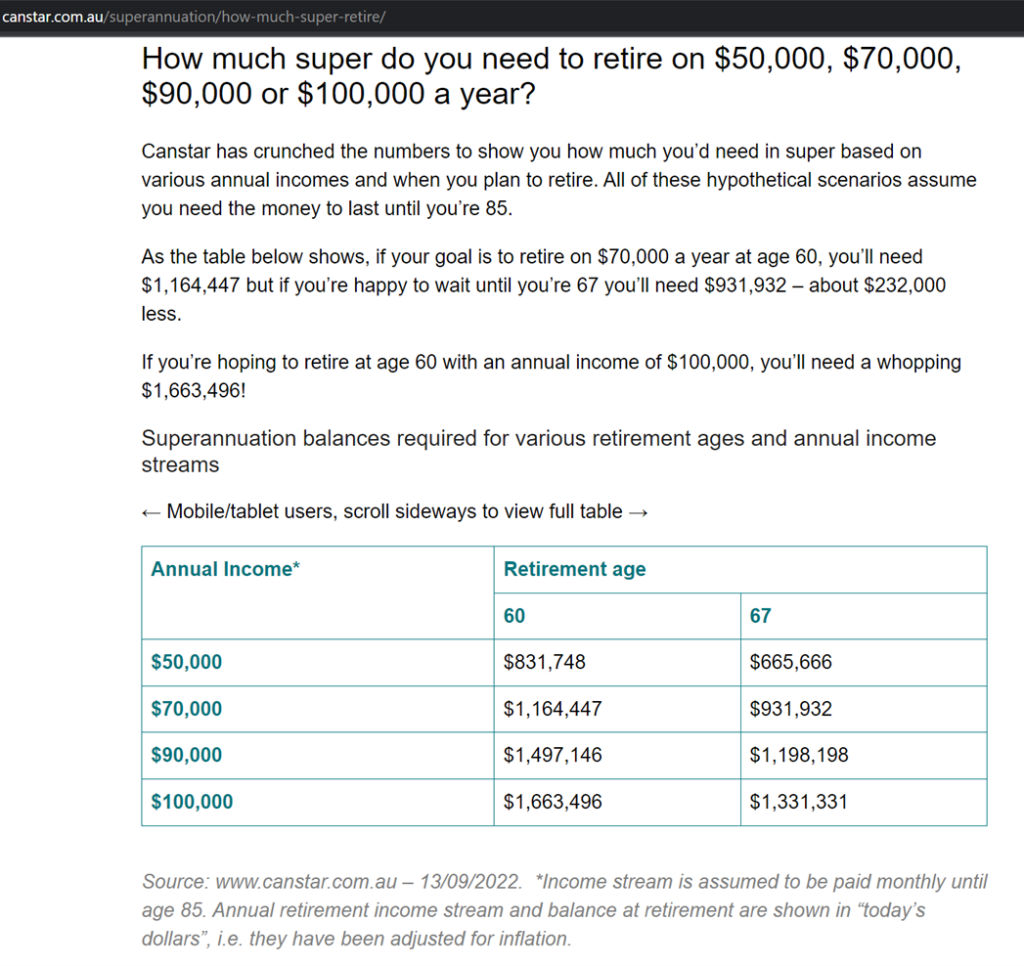

Canstar also have a similar website with valuable information on it. I found they had some great information in what age people tend to retire.

They then have some calculators on how much you would need to accumulate to draw down different income levels and at different ages of retirement.

What this calculator points out is that there is a trend that the later you retire the less capital amount you need as you will be drawing on this for a shorter timeframe.

You hear ChatGPT being mentioned and discussed everywhere at the moment so I thought I would even give it a try and see what an artificial intelligence chatbot would come up with and whilst there were some American investment references here that aren’t relevant to Australia, the general gist of what they’re saying is valuable.

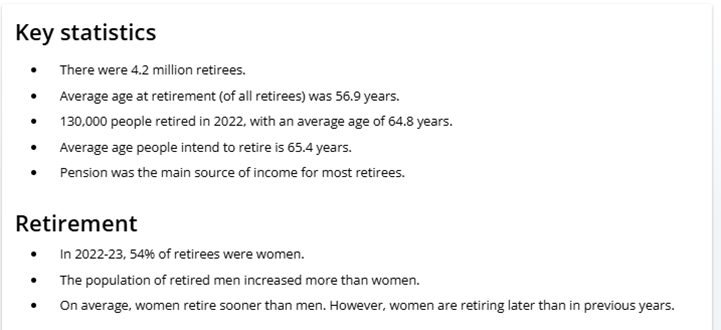

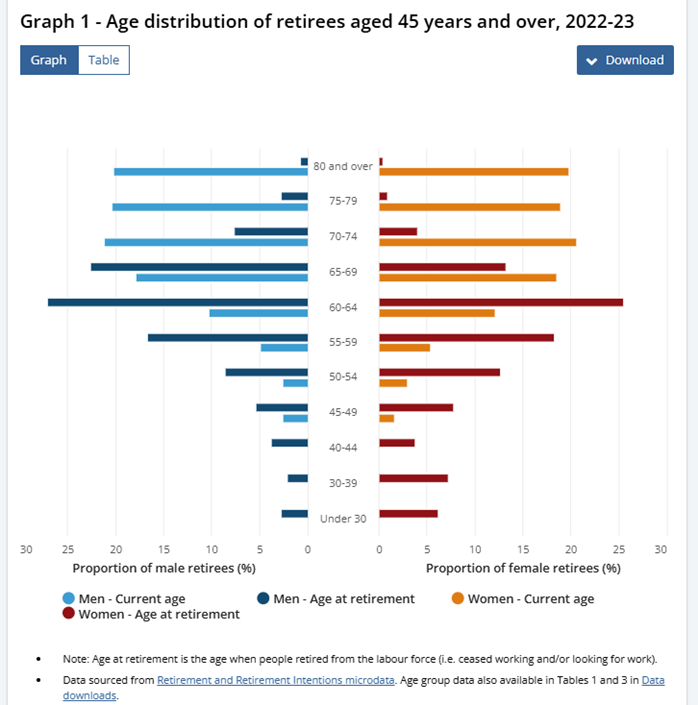

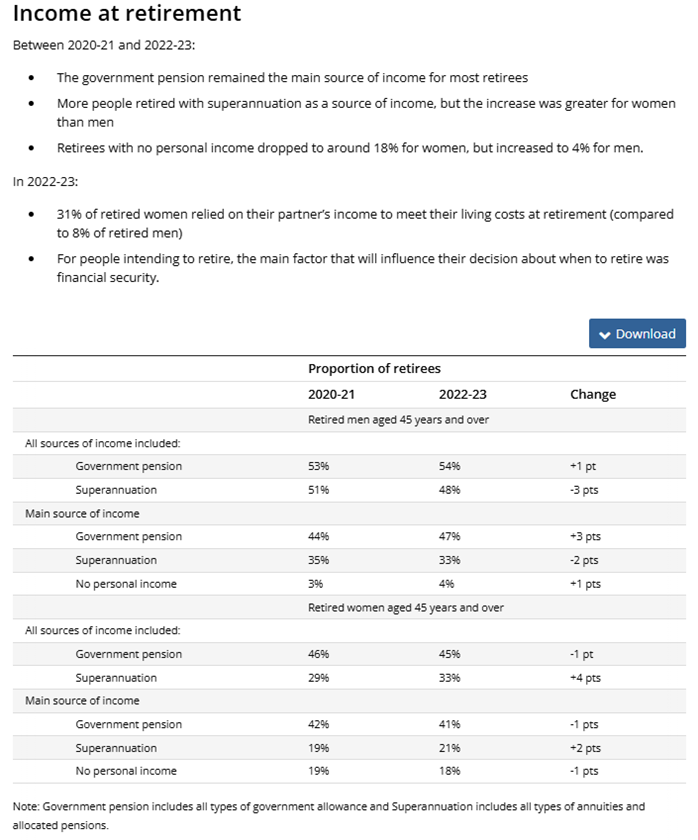

The Australian Bureau of Statistics also had some interesting retirement statistics shown as follows:

Reference period: 2022-2023 financial year

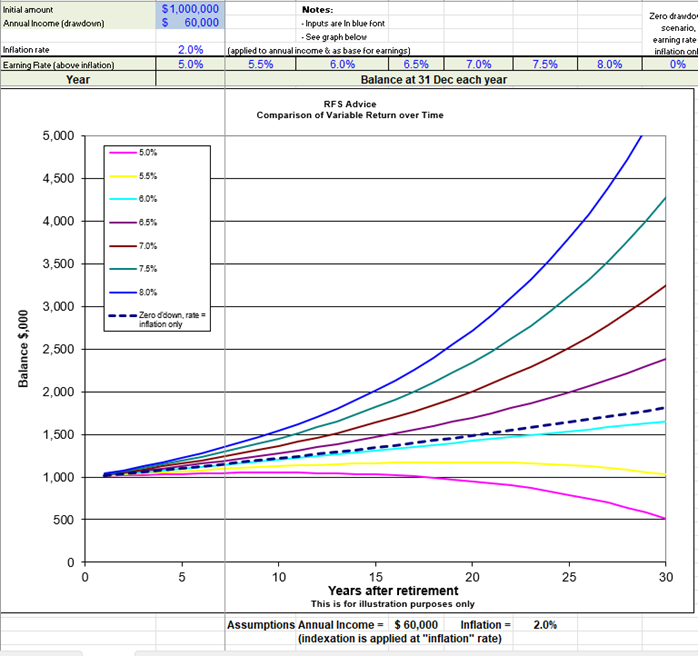

Our simple internal calculator was the final source I considered. We use this to show a basic projection of how funds can last through retirement.

For the following calculation, I used a 6% drawdown with a starting balance of $1,000,000. If you target an average return of greater than 6% in retirement and you achieve this then this should allow you to draw 6% off the proceeds and maintain your capital throughout retirement.

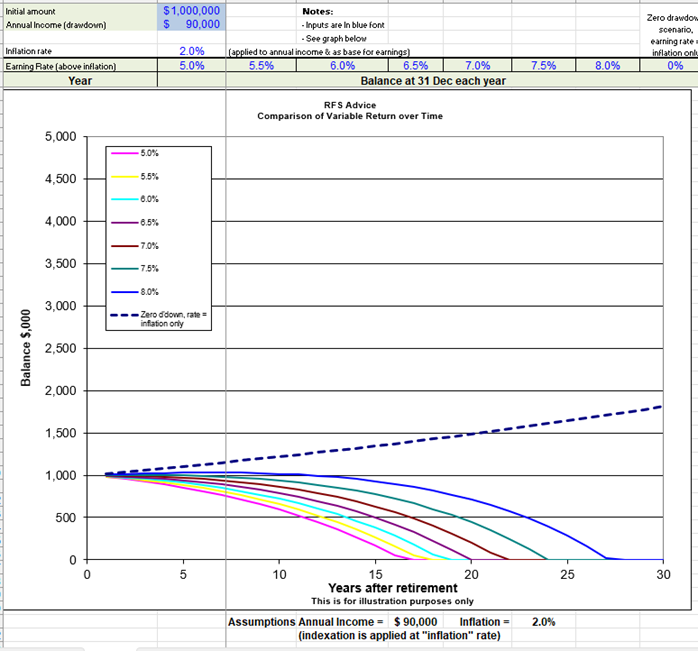

In comparison, what if you are happy to drawdown your capital over time? Let’s consider the same scenario but drawing down 9% instead of 6%.

As shown in the following output, if you draw a larger amount, your capital value will decrease over time throughout retirement (assuming the same return).

When thinking about “how much is enough”, it’s all about the right choices for your household and we strongly recommend that you take the time to plan for your retirement carefully.

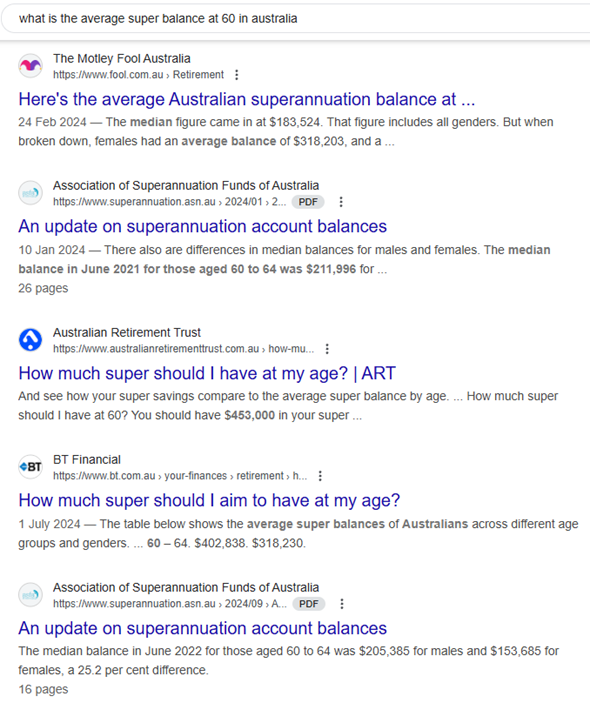

Average Superannuation balances:

Like trying to calculate how much your superannuation could be worth in retirement, there is a large range of information available on average balances. It can be hard to find an accurate comparison to see if you are on track and following is some information that I obtained from some Google searches.

In relation to what balance you should have in super now (and in retirement), the best answer is to make sure you can generate your desired income need in retirement to make sure your household is, OK. Working out these balances can be achieved with some planning and advice.

Summary Top Tips:

- You need to work out exactly how much income do you need for your household in retirement.

- What large items or trips do you want to build into your “must have bucket” in retirement?

- How will you fund your income needs in retirement?

- Where do you want to live in retirement?

- What do you want your retirement to look like in an ideal world?