General advice warning:

The information in this update is of a general advice nature only and has been prepared without taking into account your personal objectives, financial situation or needs. Because of that, you should, before acting on the advice, consider the appropriateness of the advice, having regard to those things. Past performance is not a reliable indicator of future performance and should not be relied upon.

How to Identify a Compliant Financial Adviser in Australia

When seeking financial advice, it’s crucial to ensure that your adviser is compliant with Australian regulations. A compliant financial adviser will not only help you achieve your financial goals but also ensure that your interests are protected.

We hear stories from new clients that have been to so called financial advisers, and it is disheartening to hear that there are not consistent compliant processes being applied as there are rules around what an adviser is required to do when meeting a client.

We therefore thought it would be helpful to provide listeners with some tips and traps around what to expect and what you should be looking for when meeting with financial advisers and ways that you can check that they are legitimate and following a compliant process.

1. Qualifications and Licensing

- Hold an Australian Financial Services (AFS) licence or be an authorised representative of an AFS licensee.

- Have completed the necessary education and training standards, including passing the financial adviser exam and completing a professional year (if they are a brand new financial adviser).

- Participate in ongoing Continuing Professional Development (CPD) to stay updated with industry standards.

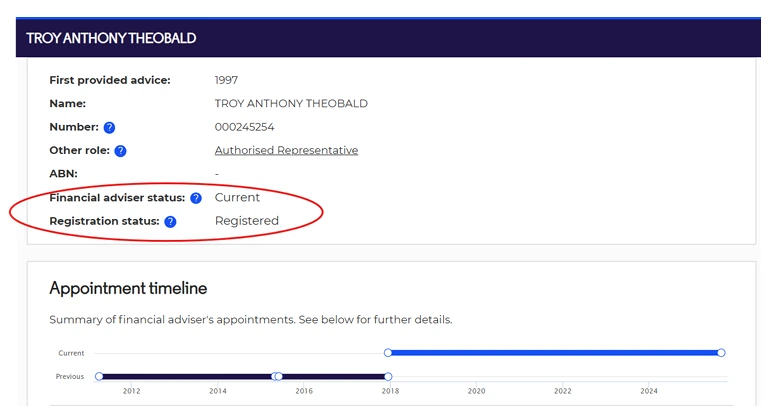

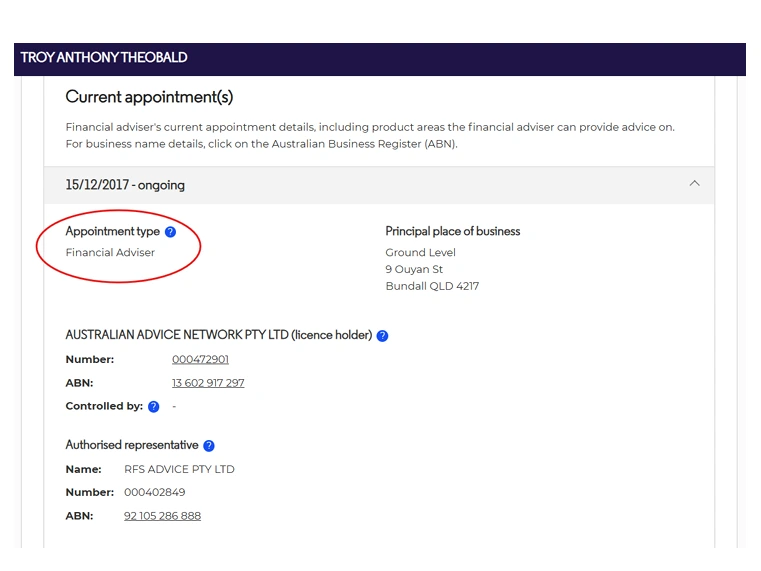

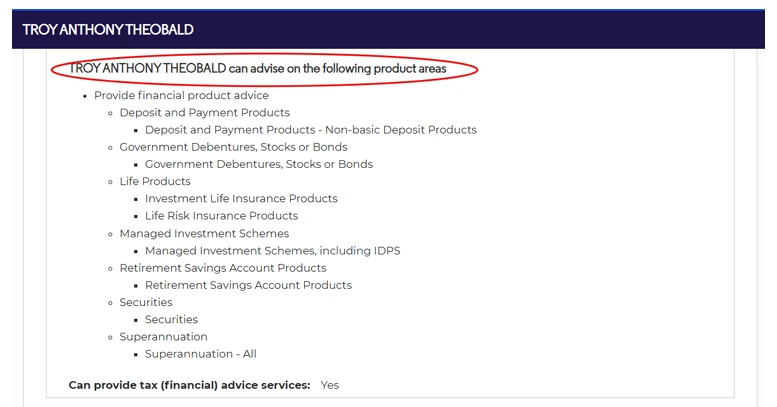

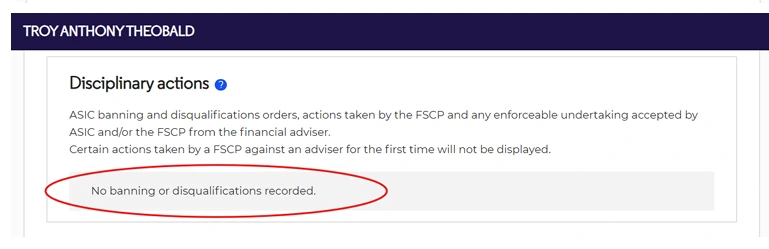

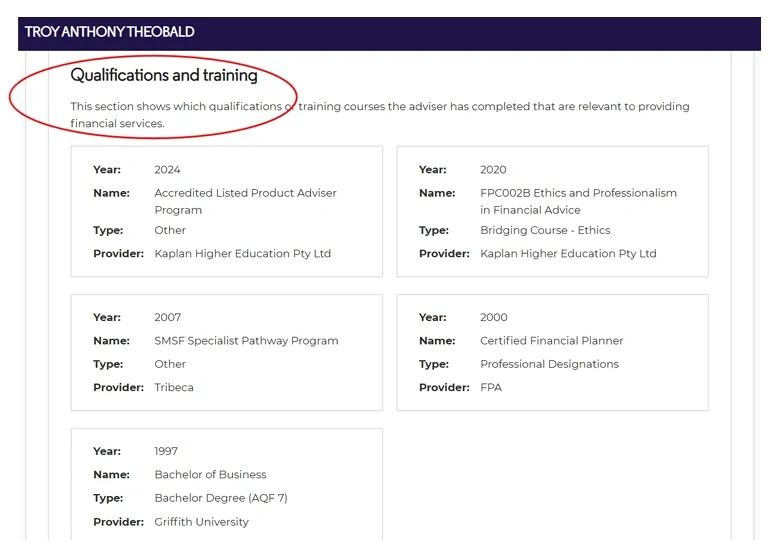

You can check an adviser’s details on the ASIC Financial Adviser Register found here: https://moneysmart.gov.au/financial-advice/financial-advisers-register

This register will show important information about your adviser such as their registration status, what they’re authorised to provide advice on, their education and whether they’ve had any disciplinary action taken against them. For example, this is a screenshot of my details and we have circled the key things to look for:

2. The Financial Planning Process

First meeting – Financial Services Guide

When you first meet with a financial adviser, they should either provide to you (or show you where to find it on their website) their Financial Services Guide (FSG).

This document contains important information to help clients understand who the adviser’s licensee is and will provide information such as:

- Who we are

- The financial products and services we can provide

- How we and other related parties are paid

- What associations or relationships we have with others that could influence the advice provided

- How we collect and use personal information

- Details of who to contact should there be a complaint

3. Getting to know each other – Client data form and Risk profile

During the first meeting it is important to get a feel for the adviser and whether you think you will be comfortable in dealing with them. An adviser will also be assessing you to all see if they believe they can assist you and whether you are someone they want to work with as well.

In order to do this, the adviser will ask personal questions in order to get a good understanding of your current situation, assets and liabilities, income and expenses and goals and objectives.

The initial meeting is probably more about where you are currently placed, where you would like to be and ideas that could help. This should not be taken to be formal advice.

Formal advice can only happen after they collect your personal details in a client data form which you should sign to verify that the information is accurate.

An adviser will also complete what’s typically called a Risk Profile Questionnaire. Throughout this process an adviser should ask you questions to assess your risk tolerance and how much risk you’re willing to take on when investing. This helps an adviser understand what Risk Profile to use and how to tailor your asset allocation when putting together an investment portfolio for you. You should be given the opportunity to review what Risk Profile that adviser has selected and agree on this or discuss any variations to it. This is a key component to the advice process and without a proper discussion you could then be placed into an inappropriate asset allocation.

Without an adviser completing both of these documents, it is difficult for them to provide you with appropriate advice that would be suitable for your needs and situation. This is a non- negotiable for a professional advice process.

During this initial meeting the adviser may also ask for third party authorities to be signed. This will allow the adviser, with your permission, to access information about your current superannuation, investments, insurance policies, tax or estate planning matters.

Information cannot be released between professionals without this privacy/third party release being signed. You should not feel pressured in the first meeting to complete a client data form and risk profile, nor should you feel pressured to sign a third-party authority if you don’t feel comfortable.

4. Questions you can ask

Throughout this first meeting this is an opportunity as previously mentioned to get to know the adviser and their business. Questions that you can ask that will help with your assessment are as follows:

- How is my personal information stored at your practice? What security processes do you have in place?

- Is my information sent to other outsourced providers as part of the advice process?

- Is any of my information sent out of Australia?

- Do you maintain an alternative remuneration register? (Soft dollar benefits that some advisers can receive) Can I see this?

- Do you have an Approved Product List? (APL) (This is a list of approved investments that an adviser is authorised to provide advice on).

- How is the adviser paid? Does anyone else receive remuneration if I invest with you? Do you personally have any conflicts with any product providers that you might recommend?

- What is the process for investments being included on this APL?

- How and where will my funds be invested?

- Are these new investments or are they established?

- How long have they been in existence?

- Is there the possibility of my funds being frozen/locked up?

- Are there independent research reports to review the investments?

- Who will I meeting with for my ongoing reviews?

- What ongoing service standard should I expect?

5. Verification Process

To comply with the Anti-Money Laundering and Counter-Terrorism Financing Act 2006, advisers must verify their clients’ identities. This process helps prevent fraud and ensures that the adviser is dealing with legitimate individuals.

This process will involve showing your identification (ie. Drivers licence, passport, etc) and your adviser will also be required to maintain a copy of this on file and provide the details to any product provider that is recommended to you.

If you are not meeting face to face (ie. Through an online meeting) then your adviser will still ask to see you hold up your ID and they will take a photo of this. You will then be required to send in a copy of your ID to the adviser for them to verify.

If you are speaking with an adviser during your meeting over the phone, then you will be required to provide the adviser with a certified original copy of your ID.

This process may not happen during the first meeting, but it must happen before any application forms are sent off.

An adviser is also required to gain an understanding into where your wealth has been generated from ie. Working life, inheritance, selling a business, investments, windfalls etc. They also need to assess source of funds for this particular investment that you’re making and how those funds are available. This could be super funds, excess savings etc.

6. Statement of Advice

After your adviser has gathered information about you, they will then prepare a financial plan for you which is called a Statement of Advice (SoA).

A Statement of Advice (SoA) is a written document that outlines the financial recommendations provided by a financial adviser to their client. It provides acomprehensive overview of the client’s financial plan, including their financial goals, investment strategies, and the recommended products and services to help achieve those goals

By law, you must receive a SoA which will set out areas such as:

- Scope of advice

- Your current situation

- Your goals and objectives

- Your risk profile

- Recommendations

- Basis of recommendations

- Product recommendations

- Alternative strategies and products that were considered

- Risks and Disadvantages

- Your recommended asset allocation

- Fees and remunerations

- Ongoing service arrangements

They will also provide you with a Product Disclosure Statement (PDS) which sets out key information about the product that the adviser has recommended.

The adviser will then have a further meeting with you to present this SoA to you. Through this meeting, it’s important to ask questions to ensure you fully understand the advice and that it aligns with your financial goals. Ensure that you understand:

- How am I paying for the advice? Is there an initial fee, implementation fee and/or an ongoing fee? Is there any commission payable? What is the frequency that I need to pay?

- If there’s an ongoing fee, what ongoing service do I receive?

- How often do I get to meet with you again?

- What happens if I have questions outside my scheduled review time?

- What are the tax implications?

- How often will you be reviewing my investments?

- Will only my bank account be linked to my accounts?

Under the Financial Advisers Code of Ethics an adviser has to be satisfied that you understand the advice before proceeding so they will be expecting you to ask questions. Therefore, don’t be afraid to ask questions and if you’re unsure of something, ask the adviser to explain it again in another way. Ask them to write it down for you or draw pictures to help explain it. You can even explain back your understanding to the adviser to ensure that you’ve understood it correctly.

A compliant adviser will never rush you, pressure you or push you into making a decision. Therefore, take the time to ensure that you understand everything and you’re comfortable to proceed. You can take the advice home to review it in your own comfort or you can get a second option if you need to.

Implementing Advice:

Once you are comfortable to proceed with the advice the adviser will have an Authority to Proceed that you will sign. If the adviser has recommended life insurance products to you there will also be an insurance consent form provided to you.

From there, the necessary application forms will be prepared and you will also sign these. As previously mentioned, if the adviser hasn’t already collected and verified your ID they will do so at this point.

The adviser will keep you informed during the implementation process and once the products are in place you will be provided confirmation letters and any applicable website login details. The product provider will also send you separate confirmation letters as well.

Reviewing the Advice:

A compliant adviser will regularly review your financial plan and make adjustments as needed to ensure it remains aligned with your goals and current economic conditions. They will also ask you questions to determine if there have been any significant changes in your circumstances and whether the recommendations and current portfolio’s need adjusting.

How often you have a formal review meeting with your adviser will depend on the ongoing service arrangement that you entered with your adviser and what was agreed upon.

Each year, if you are paying an ongoing fee to your adviser for service, then the adviser must issue you a fee consent form.

This fee consent form will outline the future fees for the next 12 months and also outline the service that you can expect to receive for this period. You are required to sign this in order for you to consent for fees to be paid and the service arrangement to consider for another 12 months.

After your review meeting the adviser may recommend that everything remain as it is with no changes or they may recommend some changes to be made.

A Record of Advice (RoA) will be completed as part of this review meeting and you are entitled to ask for a copy if you wish.

By Reference the RFS Advice process:

Our initial meeting is about capturing basic information from the client about where they are at, where they may like to get to and is this possible. It would be a general discussion around potential thoughts that should they wish to progress to formal advice we can explore in greater detail.

We also like to explain our investment process, philosophy and costing in this meeting to allow someone to come back to the second meeting and make an informed choice if they wish to progress to formal advice.

In the second meeting we would complete the client data form, go over the risk profile and have a good in-depth conversation so we understand the clients risk tolerance. Only after this and the client signing a letter of engagement would we move to formal advice and recommendations and present these at the next meeting.

At the SoA (statement of advice) presentation we would go through the formal advice to ensure this is meeting their needs and specific requirements. We want to make sure both members of a couple understand the advice and the advice process. The fees, services and any potential conflicts should all be disclosed and addressed at this time. The SoA will also clearly set out in their ongoing service agreement the services you should expect to receive, and you will be asked each 12 months to renew this service agreement.

Implementation should see you signing the documentation after having this explained to you and we encourage clients to take this home and consider it if they desire. When clients are ready to implement our recommendations, we are then required to verify and copy their ID in person. If they do not do this that is a red flag, and it needs to be verified by the adviser that is providing the advice.

When we ask clients that have received advice from other advisers that may have been poor or inappropriate advice, when we run through our process with these clients, it is evident that their previous adviser did not follow a similar process. We want this document to help provide you with a framework for the advice process. The FAAA also sets this out on their website as well.