Retirement is meant to be a time to slow down, not stress out. But for millions of Australians, it’s looking less like a reward and more like a financial cliff.

New research from Finder reveals that one in five Australians – around 4.3 million people – don’t believe they’ll have enough money in their super or investments to support themselves in retirement. Another 27% are unsure if they’ll have enough to get by.

That’s a large portion of the population entering their later years with uncertainty hanging over their financial future.

For people in their 40s, 50s and early 60s, this is a wake-up call. And while no one can change the past, the good news is it’s never too late to improve your retirement planning and set yourself up for a more secure future.

Why are so many people underprepared?

Several factors are making it harder for Australians to retire comfortably:

Rising living costs

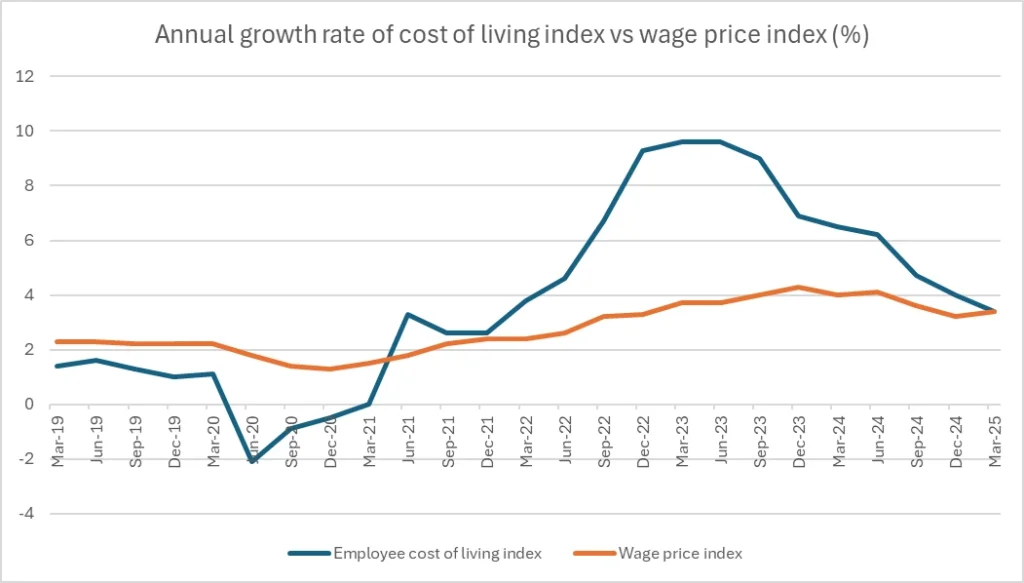

Everyday expenses have soared in recent years, putting pressure on savings and household budgets. According to the Australian Bureau of Statistics (ABS), the living cost index for an employed Australian rose 3.4% in the 12 months to March 2025. While wage growth was the same rate in the March 2025 quarter, this was the first quarter that wages rose at an equal or higher rate than the cost of living since March 2021 (see graph below).

For those still of working age, this has put severe strain on finances. The savings of many households have been depleted, and the ability to put money towards retirement is constrained by the rising cost of living. This is pushing people further away from comfortable retirements.

Mortgage stress

More Australians are entering retirement with mortgage debt, and it’s having a serious impact. Recent Roy Morgan data reveals that as of June 2025, 28.4% of mortgage holders, approximately 1.49 million Australians, were classified as ‘At Risk’ of mortgage stress in June 2025.

For those in their 50s and 60s, being at risk of defaulting on your mortgage can seriously undermine retirement readiness. Instead of boosting super or investing for the future, pre-retirees may be forced to divert income towards home loan repayments. This can delay retirement, erode savings and increase reliance on other assets. For high-income earners with significant mortgages, it also adds complexity around how best to structure cash flow, debt repayment and tax in the lead-up to retirement.

Underperforming superannuation

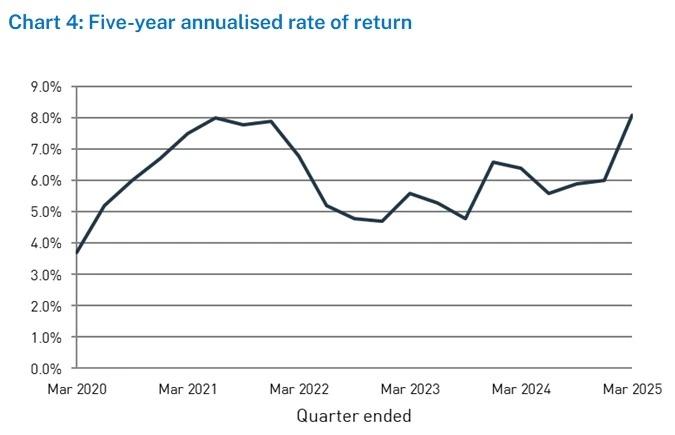

A passive or poorly managed super fund can erode your long-term wealth and impact your quality of life in retirement. Data from the Australian Prudential Regulation Authority (APRA) shows that while total super assets sat at $4.1 trillion in the March 2025 quarter and the five-year annualised return was 8.1%, not all funds perform equally. The return for the year to March 2025 was just 5.0%, and performance across choice funds varies widely.

Lack of planning

Too often, people only think about retirement once it’s just around the corner. According to Vanguard’s How Australia Retires research, one in three Australians retire without a plan and only 39% have a good understanding of the financial requirements needed for their desired retirement lifestyle.

Without a clear strategy, many risk entering retirement underprepared, with limited choices, unnecessary stress and a lower standard of living than they’d hoped for.

How much do you need to retire?

The Association of Superannuation Funds of Australia (ASFA) recommends a super balance of $595,000 for singles or $690,000 for couples to fund a ‘comfortable’ retirement. But in reality, many people have much less saved. The median super balance in June 2022 for those aged 60 to 64 was $205,385 for males and $153,685 for females.

This gap highlights the growing retirement savings shortfall facing many Australians and underscores the importance of early, consistent contributions and strategic retirement planning to avoid falling short later in life.

How can you avoid this?

It’s easy to feel overwhelmed by these numbers. But with the right strategy, you can take back control of your financial future.

First, you need to plan. But planning doesn’t just mean working out how much to save. A financial planner can also help you structure and protect your wealth. This means modelling different retirement scenarios, determining the most tax-effective way to draw income and ensuring your assets are working efficiently to support your lifestyle over the long term.

For wealthier individuals, the right adviser can help you make informed decisions around investment structures, asset allocation and timing. This is particularly important when it comes to managing taxable income, minimising the complexity of your estate and potentially ensuring any intergenerational transfers of wealth – like becoming the Bank of Mum & Dad for your children – align with your wealth goals.

Good retirement planning also looks beyond super. It considers your broader portfolio: property, shares, business interests, personal insurance and even when and how to exit certain assets. A planner can help you use your whole portfolio to build a cohesive strategy designed to withstand market fluctuations, rising costs and unexpected life changes.

Most importantly, an expert financial planner brings clarity. Rather than second-guessing complex decisions or reacting to market noise, you’ll move forward with a clear action plan, confident that your financial future is being proactively managed and refined as your needs evolve.

Retirement doesn’t have to be uncertain. With the right strategy, you can take control of your financial future and make confident decisions about what’s next. Talk to the team at RFS Advice to find out how their local expertise and personal approach to financial planning can help you build a more secure, stress-free retirement.

General advice warning:

The information and any advice provided in this article has been prepared without taking into account your objectives, financial situation or needs. Because of that, you should, before acting on the advice, consider the appropriateness of the advice, having regard to those things.