Women are re-entering the property market, showing renewed determination despite affordability pressures.

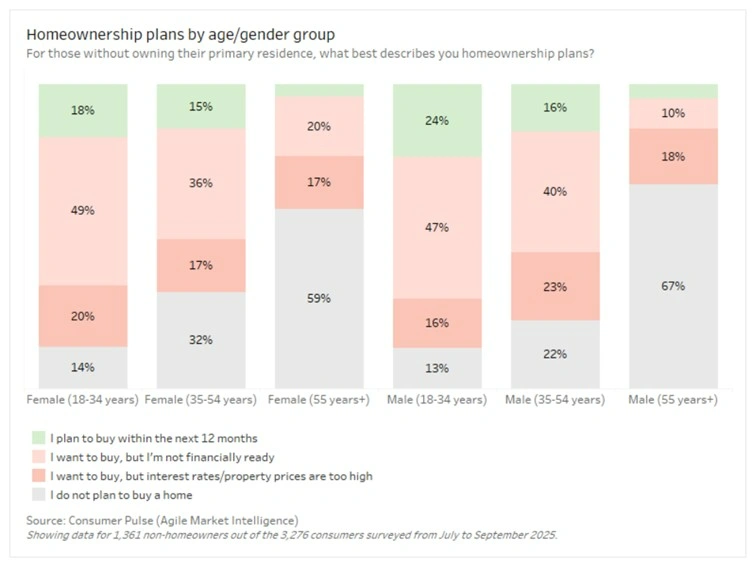

Agile Market Intelligence’s Consumer Pulse survey reveals that buying intent among women has strengthened, with both the 18 to 34 and 35 to 54 age groups recording a five-point increase in plans to purchase a home in the next 12 months. By comparison, overall buying intent across the population rose by just 1%.

The figures reveal a clear change in sentiment: women are prioritising homeownership again, even while deposit saving, high property prices and cost-of-living pressures remain formidable challenges.

The challenges women face

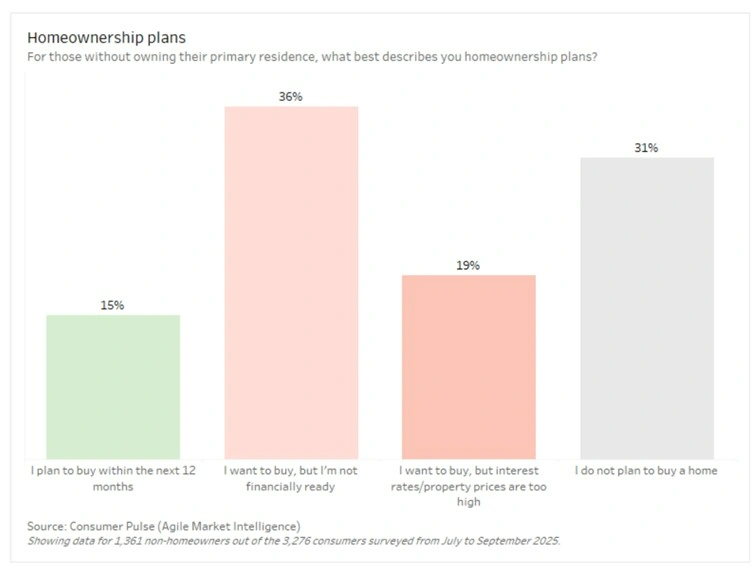

Behind the renewed optimism sit the same stubborn barriers faced by most aspiring buyers: more than half (55%) say they want to purchase but cannot. The main obstacles are financial readiness, cited by 36% of survey respondents, and the weight of high property prices and interest rates, nominated by a further 19%.

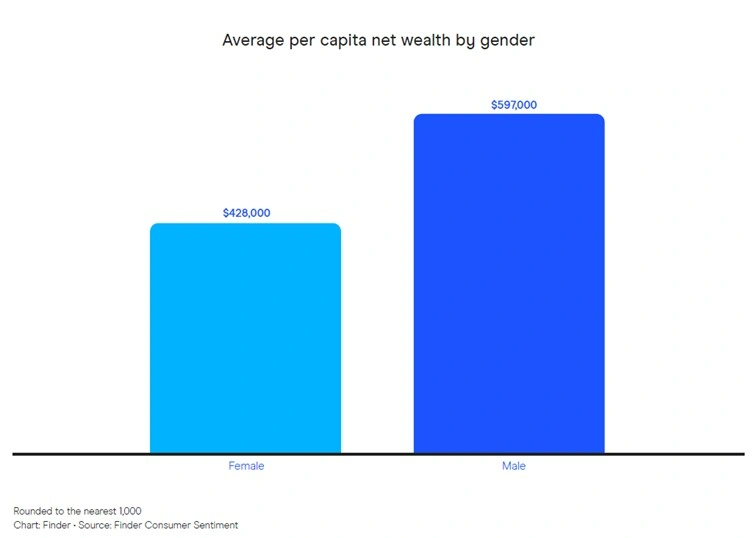

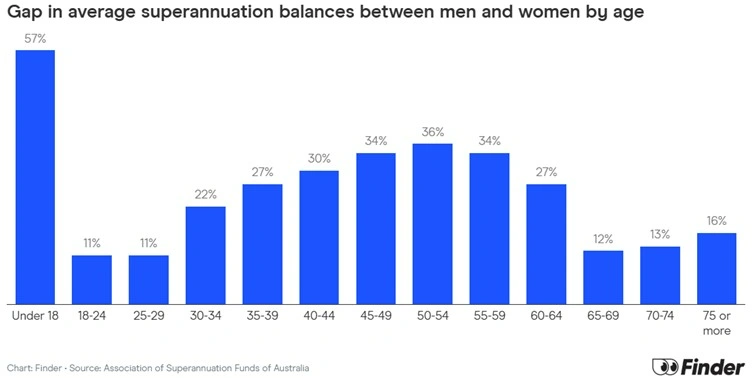

The context matters. According to Finder’s State of Women’s Wealth Report 2025, Australian women hold 40% less net wealth than men – $428,000 on average compared to $597,000. The imbalance begins early, with boys receiving more pocket money than girls, and compounds throughout adulthood due to career breaks, part-time work, and lower superannuation balances. By retirement, women are left with significantly less financial security.

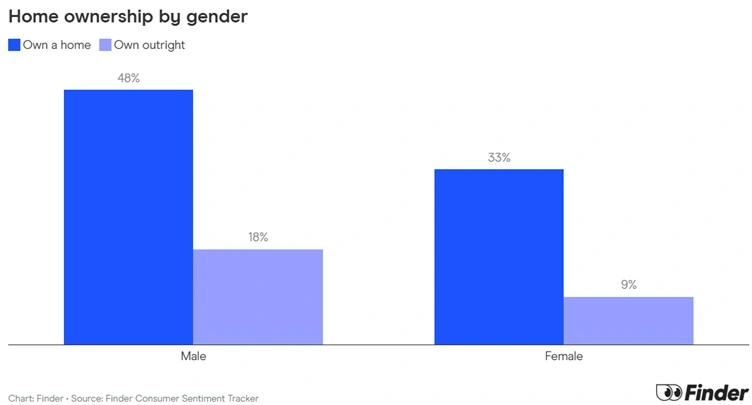

These gaps flow directly into homeownership. Men aged 18 to 34, for example, are twice as likely to own a home outright as women in the same age group (18% versus 9%). Among 35 to 54 year olds, men are also more likely to hold homes debt-free than their female peers. Taken together, the wealth gap and housing affordability pressures explain why so many women aspire to buy yet feel unable to take the next step.

Savings and deposit pressure

Saving for a deposit remains the single biggest obstacle to ownership. With Australian property prices climbing over the past decade, deposits have grown beyond the reach of many would-be buyers.

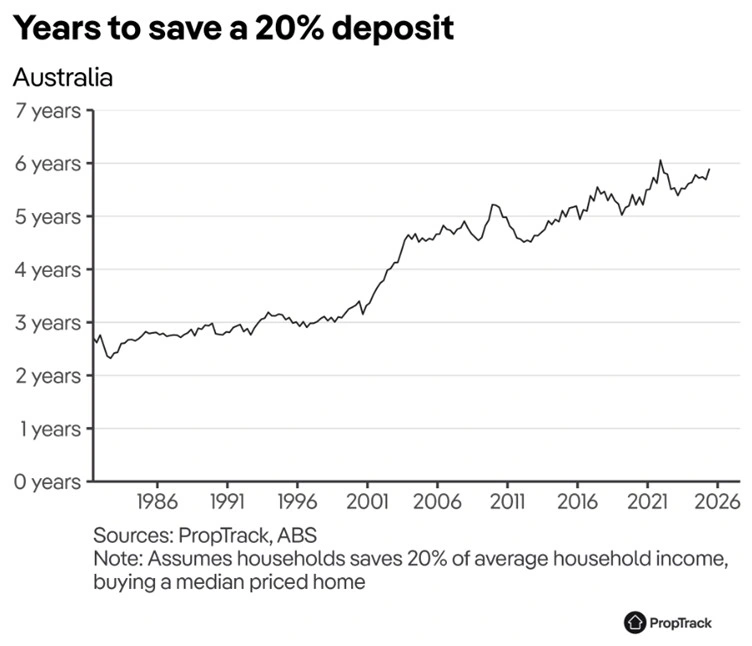

According to the PropTrack-CommBank First Home Buyer Report, an average income household would need to save for the equivalent of 5.9 years to save a 20% deposit for a median-priced home nationally.

Cost-of-living pressures have worsened the challenge: rent, food, fuel and utilities consume more of household budgets, leaving less for savings.

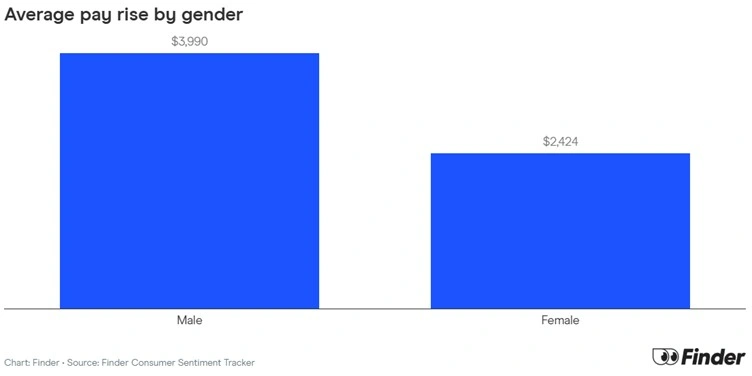

Women face additional difficulties. The Finder report shows that nearly one in three women work part time, compared to just one in ten men. Career breaks linked to caregiving responsibilities reduce earnings and superannuation, while pay rise requests are also less common among women – only 14% ask, compared to 24% of men. This combination slows wealth accumulation and prolongs deposit timelines.

Property prices and borrowing hurdles

Even when deposits can be saved, property prices remain high relative to incomes. Borrowing assessments, shaped by lenders’ obligations to ensure responsible lending, test not only current affordability but also resilience to higher interest rates. For women who may earn less on average, this can mean smaller loan approvals, effectively reducing their purchasing options.

At the same time, market sentiment remains strong. Only 31% of survey respondents said they had no plans to buy a home – a figure down from 34% earlier this year. This suggests that while affordability challenges persist, many women remain determined to achieve homeownership, underlining the importance of targeted strategies.

Strategies to move from intent to action

Structured savings

Developing a disciplined savings strategy is the first step. Automatic transfers into a dedicated savings or offset account remove reliance on leftover cash at the end of the month. Small, consistent contributions build over time, especially when paired with occasional lump sums such as tax refunds or bonuses. For many women balancing multiple responsibilities, a structured plan turns an abstract goal into tangible progress.

Government support

Government initiatives can reduce the upfront barrier. The First Home Guarantee allows eligible buyers to enter the market with just a 5% deposit, while avoiding the cost of Lender’s Mortgage Insurance. These schemes effectively shorten saving timelines by cutting the required deposit amount, which can be particularly valuable for women who are otherwise forced to delay entry into the market. Checking eligibility and local price caps early ensures that saving goals align with program limits.

Professional advice

Seeking expert guidance can make a significant difference. Working with a financial planner or a Gold Coast financial adviser provides clarity on how a property purchase fits into an individual’s overall financial picture. This advice can help women structure their cash flow, optimise savings and borrowing strategies, and ensure that buying a home does not compromise other financial objectives such as retirement planning and savings.

Why alignment with long-term goals matters

Owning a home is often seen as a cornerstone of financial stability. But for women, whose lifetime earnings and super balances remain lower than men’s, it is crucial to view the purchase in the context of broader financial planning.

A well-considered purchase should:

- Provide long-term security and stability

- Reduce housing costs in retirement by eliminating rent

- Complement superannuation and investment portfolios

- Fit within personal risk tolerance and cash flow needs

The danger of treating a property purchase in isolation is that it can lead to financial strain later. By contrast, aligning homeownership with long-term goals helps ensure that the home contributes to wealth creation and retirement security, rather than competing with them.

Broader implications for women’s wealth

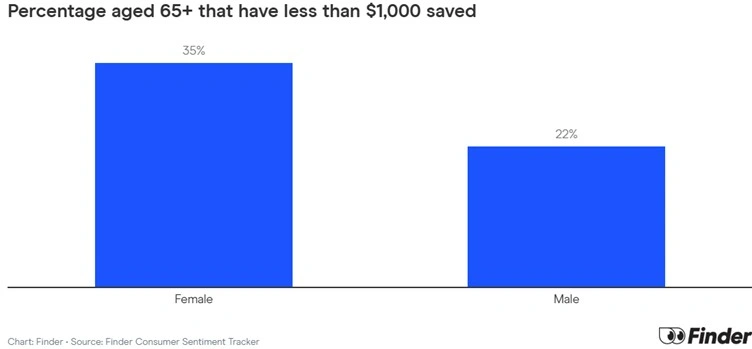

The Finder report highlights that 35% of women over 65 have less than $1,000 in savings. This stark figure reinforces the importance of women engaging proactively with money decisions earlier in life, including property ownership.

Housing remains one of the most powerful tools for building wealth in Australia. For women, entering the market – even with challenges – can set the foundation for improved long-term outcomes. It provides not only stability but also an asset that can support wealth accumulation across decades.

Take the next step

If you are considering homeownership, RFS Advice can help you turn intent into action. Our highly educated advisers support women at every stage of life, ensuring property ownership fits seamlessly into a broader financial planning strategy.

By integrating savings, borrowing, investment and superannuation into one plan, we can help you achieve your goals with confidence. Contact RFS Advice today to speak with a Gold Coast financial adviser about your financial future.

Frequently asked questions

Australian women hold around 40% less net wealth than men on average, according to Finder’s State of Women’s Wealth Report 2025. This means women often face longer deposit timelines, lower borrowing capacity and less financial flexibility, making professional advice and structured planning even more important when aiming for homeownership.

Structured savings plans, automatic transfers and higher-interest accounts can help. Government schemes can also reduce the required deposit.

Eligible buyers may access schemes such as the First Home Guarantee, which allows purchases with a 5% deposit and no lender’s mortgage insurance.

A financial planner can ensure a property purchase aligns with long-term goals, cash flow, and risk appetite.

Yes. A home provides stability and reduces costs in later life, but it should be considered alongside superannuation and other investments for a balanced strategy.

The information and any advice provided in this article has been prepared without taking into account your objectives, financial situation or needs. Because of that, you should, before acting on the advice, consider the appropriateness of the advice, having regard to those things.