Recent months have seen several large employers across Queensland, including on the Gold Coast, announce job cuts.

The Gold Coast City Council, for instance, has launched a voluntary redundancy program for up to 600 staff, aiming to cut around 100 positions as part of a $75 million cost-saving initiative. These measures include improved rostering and operational efficiencies.

At the start of 2025, the Nine Network confirmed job losses at its Gold Coast bureau. Just a few months later, the Downer Group, which is contracted to build 65 passenger trains for Queensland Rail ahead of the games, warned staff of potential redundancies at its Maryborough facility and began consultations.

The University of Southern Queensland recently also revealed plans to cut 150 jobs. This is in addition to the termination of 109 roles in 2024, including 85 redundancies and 24 pre-retirement arrangements.

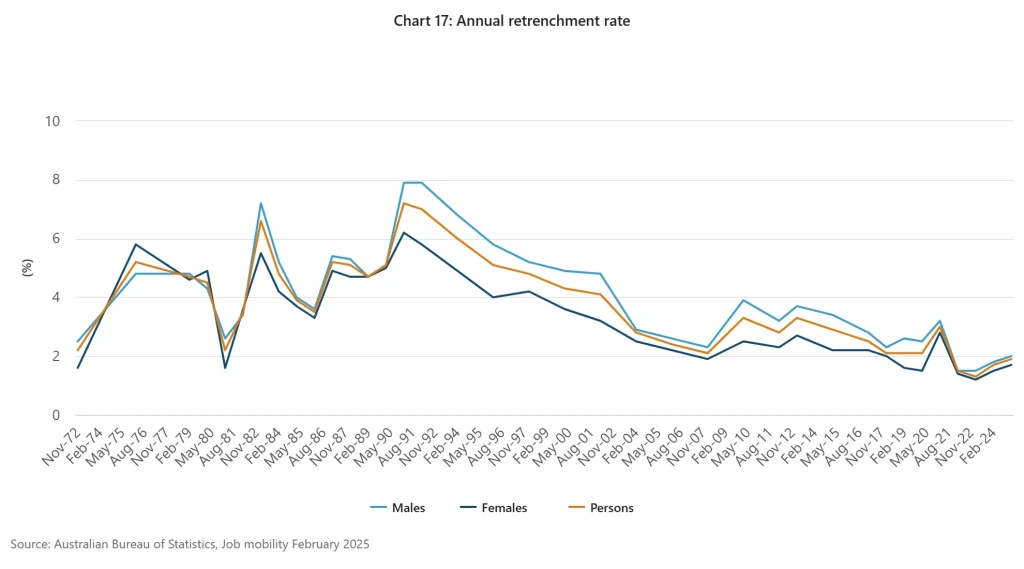

Across the state, retrenchments are on the rise. According to the Australian Bureau of Statistics, 57,500 Queenslanders were retrenched in the year to February 2025, up from 43,400 the year before. This was the highest annual figure since the Covid pandemic, when 79,400 retrenchments were recorded in the 12 months to February 2021.

Nationally, 268,100 Australians lost their jobs through retrenchment over the same period. This represents a retrenchment rate of 1.9%, up 0.2 percentage points annually.

These numbers highlight a reality that many professionals now face: redundancy is no longer a rare event.

Yet for those who have recently lost their jobs, or face the possibility of being let go, redundancy can also be reframed as a catalyst for change – a moment to take stock, explore new directions and lay stronger foundations for the future.

Step back and assess your position

When a role ends, the immediate instinct may be to rush into the next available opportunity. But redundancy offers a unique chance to pause and assess where you stand. This means asking questions such as:

- What financial commitments do I need to cover in the short term?

- What parts of my previous role energised me, and which drained me?

- Am I looking to stay in my industry, or is this the time to make a career change?

Working with a financial planner can provide clarity at this stage. By mapping out income needs, assets, debts and lifestyle goals, it becomes easier to make decisions that align with both your financial and personal objectives.

Identifying your skills, passions and opportunities

A redundancy is often the prompt to reassess your position, not just of finances but of professional skills and interests. This review can uncover opportunities that may have been overlooked in the stability of a previous role.

Practical steps include the following self-assessments:

Skills audit

List technical skills, transferable capabilities, such as leadership, problem-solving or project management, and any areas where you have specialist expertise. Recognising transferable strengths is particularly powerful as it can reveal openings in industries that may not have been on your radar before.

Passion check

Consider which activities you find most meaningful and motivating, both in and outside of work. Aligning your next career move with your interests not only increases satisfaction but can also lead to more sustainable long-term success.

Opportunity scan

Research growth industries and roles in demand, including those highlighted by government skills shortage reports. By matching your skills and passions to areas of genuine demand, you increase your chances of finding stable employment and building a career with future resilience.

The chance to pivot, upskill or start something new

For some, redundancy has proven to be an opening to pivot into a new career path, upskill or even start a business. Options include:

Pivoting industries

Many professionals discover that their core skills are transferable to sectors experiencing growth, such as healthcare, technology or renewable energy.

Upskilling

Short courses, diplomas or postgraduate study can position you for higher-demand roles. The federal government’s National Skills Commission regularly publishes priority skills lists.

New ventures

Some choose to invest redundancy payouts into small businesses or start-ups, provided this aligns with their financial capacity and risk tolerance.

A Gold Coast financial adviser can help assess which option aligns with your long-term wealth and lifestyle goals.

Making redundancy payouts work for you

A redundancy payout can feel like both a relief and a challenge. For many, it arrives as a lump sum larger than any previous pay cheque, and the instinct may be to treat it simply as a buffer until the next role appears. While it certainly provides short-term security, its real value lies in how it is managed for the future.

Covering immediate needs first

The first step is ensuring that immediate needs are covered. Setting aside enough to pay essential living expenses for several months helps reduce stress and creates space to make clear-headed decisions about what comes next. Once this safety net is in place, a payout can become a foundation for longer-term goals.

For some, this means boosting superannuation.

For example, someone aged 55 who receives a $40,000 genuine redundancy payment could, subject to eligibility and contribution caps, direct a portion into super to accelerate retirement planning. The ATO explains that genuine redundancy payments are tax-free up to a limit based on years of service, indexed annually from 1 July.

Making a well-timed contribution can have a compounding impact over the final working years before retirement.

Reducing debt to create stability

Others may see greater value in reducing debt. Using a payout to clear loans or credit cards with high interest rates can deliver immediate savings and free up future cashflow.

For example, a 42-year-old with a $25,000 payout might first eliminate high-interest debts to improve financial stability, then allocate a defined amount towards retraining and further education if needed.

This combination of debt reduction and upskilling provides both short-term relief and new long-term opportunities.

Turning payouts into long-term growth

For those already financially stable, investing part of a payout may be another pathway to growth, provided the level of risk matches personal circumstances. The crucial point is that redundancy payments should not be seen as an end in themselves, but as a tool to support future choices, whether that means retraining, starting a business or preparing for retirement. Partnering with a highly educated financial planner or a Gold Coast financial adviser ensures that every dollar of a payout is aligned with a structured financial plan, rather than spent reactively.

Frequently Asked Questions: Redundancy and financial planning

Take time to review your immediate financial needs, including living expenses, debts and upcoming commitments. Speaking with a financial planner can help you understand your options clearly.

Your payout should be treated as a strategic resource. Cover essentials first, then consider debt repayment, superannuation contributions or investments. Advice from a Gold Coast financial adviser can ensure you make decisions that align with long-term goals.

Yes, redundancy can be a springboard for change. Conducting a skills and interests audit, exploring growth industries, or considering retraining can open up rewarding new paths.

While not essential, many people benefit from advice. A financial planner provides guidance on budgeting, investing and structuring payouts, while also helping you balance short-term needs with long-term financial planning.

Take control of your next chapter

Redundancy is never easy, but it can also be the start of a stronger future. By reviewing your skills, exploring new opportunities and using your payout wisely, you can turn job loss into growth.

If you are navigating redundancy on the Gold Coast and want clarity on your financial direction, reach out to RFS Advice’s team of highly educated advisers. We can help you make confident, well-informed choices.

General advice warning:

The information in this blog is of a general advice nature only and has been prepared without taking into account your personal objectives, financial situation or needs. Because of that, you should, before acting on the advice, consider the appropriateness of the advice, having regard to those things.